Table of Contents

Next.js Development

Build blazing-fast, SEO-friendly React websites and apps

- ✔️ Server-side rendering & static site generation

- ✔️ Built-in routing and API support

- ✔️ Optimized for performance and scalability

- ✔️ Ideal for modern web apps and marketing sites

![]()

As of 2021, only 0.5% of the population uses blockchain technology.

Before you jump to conclusions, it is not a commentary on the usefulness or trustworthiness of the technology. Like every other emerging technology, blockchain has a long way to go before widespread adoption propels to perpetual usage. Yet, the global spending on blockchain increased to 6.6 billion USD in 2021. Hence the estimate is that 80% of the population will be involved with blockchain technology within ten years.

While blockchain is widely popular for being the foundation of cryptocurrencies, it has a lot more to offer for various industrial sectors. According to Gartner, Blockchain has such a major impact on businesses that it is considered the second most disruptive technology in recent times, after artificial intelligence and machine learning.

So, entrepreneurs and executives will need to get on the blockchain bandwagon to stay ahead of their competitors. If you too are thinking about making this shift, take a look at some of the major advantages and disadvantages of blockchain technology that you should consider moving forward.

Table of Contents

Things to Know About Blockchain Technology

Also known as distributed ledger technology, Blockchain is the decentralized technological foundation of most digital assets today. Many would even say that blockchain is a way of recording things in a way that cannot be tampered with or cheated with. Blockchain is a network of computers in which information is stored in the form of a digital ledger of transactions.

The record of each transaction is added as a block to the network and is created as to the ledger of every individual on the network. Any change to this block would be quite apparent and would require making changes to every block on the network, making the system secure and difficult for hackers to manipulate. Apart from this, one of the major factors that define the security of the blockchain is the fact that it is not run by an individual or company, and is instead governed by the people who are using it and are a part of the network.

The goal of blockchain is to have an immutable ledger thus safeguarding the transactions recorded in the network. It is this level of security that makes it the perfect foundation for smart contracts, which are contractual terms laid down in a way that they can not be edited without changing all the blocks related to them. Thus, the technology aids in reducing fraudulent transactions and related mistakes significantly.

#1. Use Cases

Industries and processes that require a higher level of security and transparency for transactions are some of the most prominent use cases for blockchain technology. Blockchain is also the ideal option for industries that require digital assets to have a higher level of security and performance.

With that in mind, here are a few popular use cases of the technology:

- Cryptocurrencies: The most popular and known application of blockchain technology is of course, in the form of cryptocurrencies. Blockchain helps cryptocurrencies to record a ledger of payments transparently and allows them to operate without a central authority. Moreover, it also significantly reduces risks associated with cryptocurrencies, and the related processing and transaction fees.

- Defi: Decentralized Finance, a digitized version of traditional finance, is a way for potential investors to put money into digital assets, without the intervention of any central financial authorities or regulations. It allows individuals to invest and avail of loans while cutting down on the predominant paperwork that is otherwise required.

- NFTs: Non-Fungible Tokens, are a way for individuals to establish ownership of unique items such as collectibles and artworks, through blockchain. It is taking the world by storm as people across the world, even artists from low-income countries can leverage this concept to their advantage.

- Supply Chain: Blockchain is used in supply chain strategies and processes to increase transparency and improve the way data transfers are done with improved accuracy. It is a great upgrade over the traditional approach since it allows companies to eliminate some of the common errors and lags while enhancing overall fulfillment solutions.

- ID Verification: At the very foundation, Blockchain can transform into a data registry that is highly secure, verifiable, and tamper-proof. In terms of identity management, blockchain can empower everyone in the network to verify the credentials of each user without any room for errors.

- Internet of Things (IoT): IoT combines with blockchain to create and share tamper-proof records of transactions across various devices on the same network. The integration of blockchain in IoT makes it more efficient, highly flexible, and grants additional security. Not only this — you can make your data even more trustworthy and increase interoperability between devices.

Advantages of Blockchain Technology

We have discussed some of the major advantages that blockchain technology has in store for users and investors so far. Let us take a deep dive into how you can leverage these advantages.

#1. Higher Security

This might sound a tad repetitive, but one of the biggest advantages of blockchain technology is the increased level of security. Regardless of the application, blockchain can be used to create permanent and immutable records of important data and information.

Firstly, all blockchain transactions are stored using cryptography. Every block is identifiable using a highly secure and private key, which can be verified with the help of a public key. In case the data related to the transaction is edited or tampered with within the block, the private key assigned to it becomes invalid, and the block gets removed from the chain.

Moreover, the public nature of blockchain makes it difficult for malicious parties to make any changes to the network. Any minor or major changes can be verified with the help of the public key, and become immediately apparent to all the systems in the entire network, thus reducing the possibility of a hacking attempt.

Even then, some major hacks with devastating consequences have happened, such as the one on Mt. Gox where hackers were able to steal nearly 900,000 BTC (6 billion USD in today’s value). However, such incidents often result from a lack of internal policy regulations and security measures.

#2. Increased Transparency

Whether it is about fetching customer insights or transactions, ensuring transparency can be mutually beneficial for companies and their customers.

The good news is that transparency and security go hand in hand when it comes to blockchain technology. It also helps that the very goal of blockchain technology is to make transaction and data management more transparent.

First of all, the decentralized nature of blockchain technology means that each block or ledger that is added to the blockchain network will be distributed and shared with each system in the network. This mechanism extends transparency to the extent that each system on the network will be able to monitor and see any changes happening in real-time

Moreover, records that have been added as blocks on the network cannot be hidden or altered in any way. Editing or deleting the records on a blockchain network will create a record of the action, which will store all the information about who carried out the edit or deletion, and what was lost or added in the process.

#3. Better Traceability

Again, the transparent nature of blockchain has a lot to do with the approach it takes toward improving traceability. As we have already seen, blockchain can be used in various industries and processes to upgrade their security and transparency.

This is possible because blockchain makes it easy for users to find audit trails for specific and all transactions. This is revolutionary for several industries, especially for the consumer goods industry.

Tracing transactions and ledger records is a major advantage when it comes to determining provenance in the supply chain. For instance, managers can trace the journey of a food item from the source of origin to the destination seamlessly with the help of blockchain technology. Some businesses and industries struggle with ensuring end-to-end traceability even if it is necessary for ensuring quality. Industries that are vulnerable to counterfeiting or fraud can especially leverage blockchain to provide proof and trace the origins of any such issue.

#4. Improved Speed

Image Source: Wealth and Finance International

One of the biggest challenges associated with traditional paper-based transactions is that they take a lot of time, and more importantly, prove expensive. Such processes are also vulnerable to human errors, and end up costing companies a lot if not monitored accurately.

All the transaction details and related documentation can be stored on the blockchain eliminating the need for companies to do additional paperwork. Smart contracts are also known to be more reliable and secure compared to paper contracts, with higher processing speeds.

These features lead to improved transaction and processing speeds, making it a great choice for fast-paced agencies and businesses that run and earn primarily on contracts.

Even as an individual investor, you have the added advantage of leveraging some of the common crypto paper trading apps, which let you simulate real trading transactions without losing real money.

#5. Complete Automation

Empowered by blockchain, smart contracts eliminate the need for middlemen to enforce and manage contracts. Smart contracts also eliminate the need to hire additional personnel for background checks and verification.

Organizations today strive to automate processes more than ever, for increased efficiency. Right from SEO services to financial transactions, companies have a growing need for automation so that processes can be more streamlined.

Automating processes can help your business in multiple ways. It can not only reduce your costs but also the time is taken to fulfill important processes.

#6. Versatility

One of the most prominent advantages of blockchain technology is how versatile it is proving to be for companies and industries of all sizes and types. Blockchain can prove to be a great asset in terms of facilitating transactions, contracts, as well as managing processes efficiently.

If integrated effectively, it can be a great way to upgrade the performance of several types of companies, and make their processes more secure and accurate.

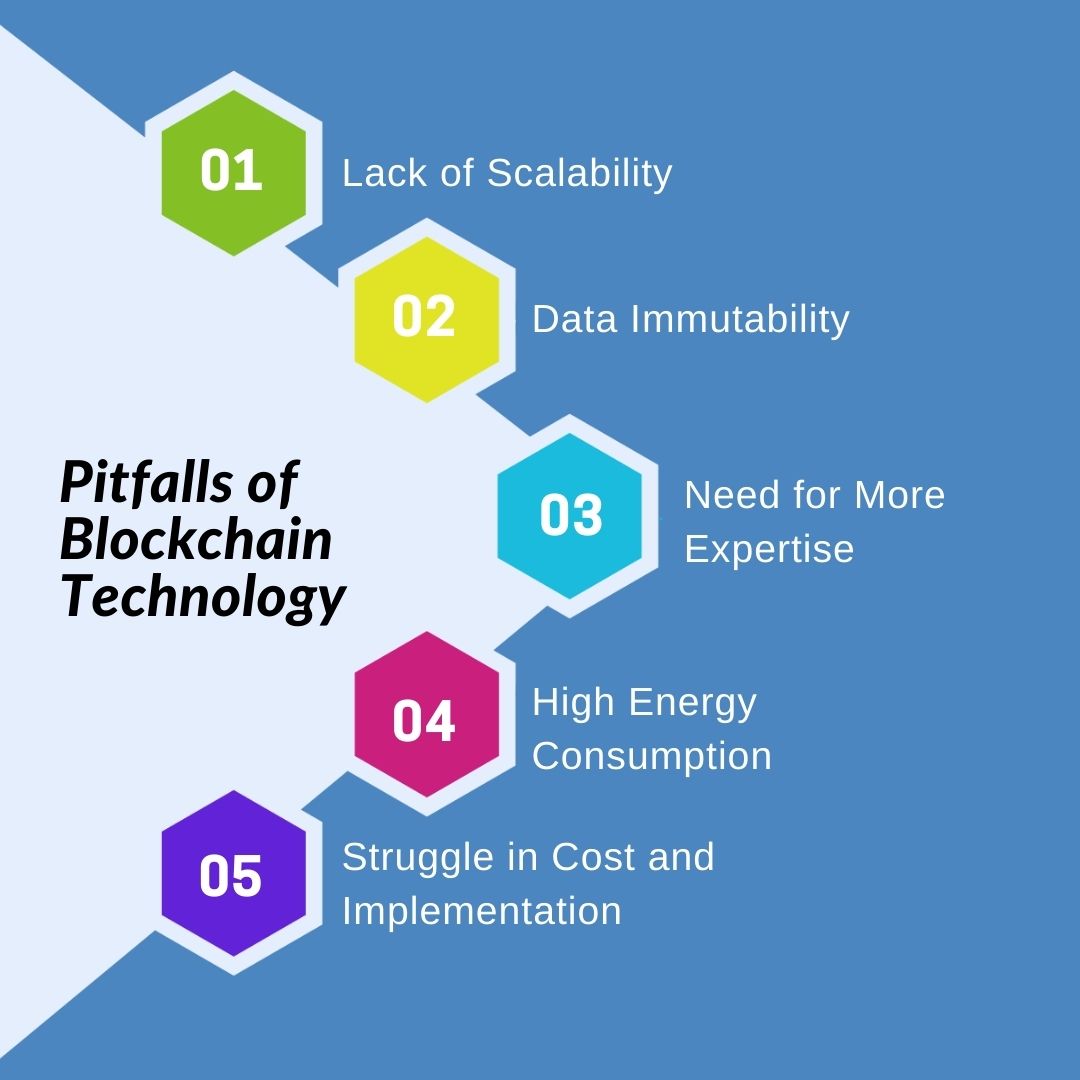

Pitfalls of Blockchain Technology

It is important to remember that blockchain is a new technology and the world is still discovering the many capabilities and vulnerabilities that it has. Now that you know all about the major factors that are in favor of blockchain, here are a few pitfalls that will give you a comprehensive understanding of how to go about implementing it.

#1. Lack of Scalability

Out of the few challenges that blockchain still poses for companies, one of the major ones is technical scalability, especially in public blockchain networks. This is also one of the issues that are putting a strain on the more widespread adoption of the network globally.

To put this in perspective, consider the fact that a major payment provider such as Visa processes roughly 2000 transactions every second. On the other hand, the most popular cryptocurrencies such as Bitcoin and Ethereum that run on the blockchain can only process around 3 and 20 transactions per second.

When we talk about such transaction speeds within a private blockchain consisting of only a few trusted parties, this actually works to their advantage. But for widespread adoption, there is a dire need for mechanisms that increase the number of transactions such networks can process. This is also one of the reasons why Ethereum, which is the foundation of Defi, is considering moving to a consensus mechanism (proof-of-stake), which will make transactions faster, and networks more scalable.

#2. Data Immutability

While data immutability has often been cited as one of the major advantages of implementing blockchain, it is also one of the major pitfalls of the technology. Immutability has time and again proven valuable for systems such as supply chain and financial systems, but for other industries, it can be quite daunting.

But this immutability is only possible if the nodes are distributed fairly across the network. A blockchain network where an entity has ownership of more than 50% of the nodes can actually be quite vulnerable.

Another important drawback of immutability is that it completely ignores the privacy aspect. Every individual is entitled to their privacy, but even then, blockchain does not allow data that is written to be erased. So if an individual had published information on the blockchain at a specific time, and no longer wants it to be there, there is no way to grant that privacy to them, without letting every single person on the network know.

#3. Need for More Expertise

Blockchain may have good things in store for you once you get a hang of it, but the process of getting there requires you to learn all about this nascent technology. For an individual who is not from a tech background, understanding how blockchain works can be quite stressful, but once you do, you would be able to leverage it to make your processes more efficient.

Organizations would need to start by experimenting with single-use applications of blockchain, and understanding it comprehensively before taking it to a more advanced level. The need for learning these skills can be a significant challenge in carrying out company processes and systems, which is also a major reason for the low blockchain adoption rates in many industries.

#4. High Energy Consumption

As is the case with every emerging technology, setting up for blockchain requires companies to consider the hefty setup and costs associated with such an infrastructure. But as for high energy consumption, it is a little bit of a myth. The high energy costs that people are often quick to associate with blockchain are almost entirely because of the energy consumption that Bitcoin requires.

While setting up a hefty infrastructure for implementing blockchain can definitely cause a surge in your energy consumption costs, it has for the most part helped the climate action as opposed to having negative consequences on it. Additionally, when you sell bitcoin using blockchain technology, the process remains secure, transparent, and decentralized, ensuring a seamless transaction experience.

Many environmental agencies and representatives use blockchain to create transparent and powerful campaigns. So while individual companies might actually need to be wary of the inevitable surge in their energy consumption, the technology is a safe bet from a holistic point of view.

#5. Struggle in Cost and Implementation

Considering the expertise required for blockchain to be implemented in an organization, and the infrastructure required to support it, it is no surprise that the costs are quite high. In most cases, one of the persistent challenges that corporations face is the difficulty in integrating the technology with their existing legacy systems.

Most businesses need to contemplate a complete IT systems upgrade when moving to blockchain technology which can not only be expensive but also require a solid implementation strategy. Even then the possibility of data breaches and loss during the transition can be highly demotivating for companies.

Then there is the dearth of blockchain developers in the market today, making the ones that are available quite expensive. The need for such expensive investments has been discouraging businesses from taking the plunge for quite a few years no

Summing up

Blockchain undoubtedly has a firm place in the future of many businesses and industries worldwide, however, it is important to consider that like any nascent technology, it has its share of challenges. Having said that, if implemented effectively, businesses can truly unlock the potential of blockchain technology and all it has to offer for companies worldwide. Apart from the use cases that we have discussed here, the adoption and applications of blockchain are only set to grow in the foreseeable future.